So You Want to Be a Fund Manager?

So You Want to Be a Fund Manager?

Life comes at you fast

To my 76 new mates, welcome to issue 31! As always, keen to share what I’ve been reading, learning, and compressing. A quote from Anthony Bourdain to start:

I understand there's a guy inside me who wants to lay in bed, smoke weed all day, and watch cartoons and old movies. My whole life is a series of stratagems to avoid and outwit that guy.

Here’s the format of today’s email:

Part 1: So You Want to Be a Fund Manager?

Part 2: Bonus Quirky Content - Something to Read, Watch, and Listen

So You Want to Be a Fund Manager?

I’ve previously touched on investing as a business in issue #18. But have found a few more resources and links that deserve to be dissected and shared.

Letter to a friend who may start a new investment platform [Link]

Graham Duncan covers seven questions you should answer before starting a fund. Topics like having a spouse fully onboard, sourcing ideas, and keeping ya head screwed on.

Being able to always see the downside in a situation is slightly easier when you’re an analyst, but when you’re the leader of a new enterprise, it’s important to transmit the message to your internal and external partners that while failure is of course possible, you’re going to do everything you can to will the new initiative to success. So you have to practice asserting reality in advance.

I love the above quote because it’s something I think about often. Because in investing you need to constantly prepare and thinking about ways of failure. But if you’re running a business or a sportsman, you can’t consider failure if you’re going to succeed. Failure can’t be an option because if you let negative scenarios creep in it’ll kill you. But if you’re an investor who doesn’t consider failure, you’ll get killed! I think that’s why I find running an investment business so interesting because you need to manage both sides so well.

In life and business, “approach” goals are much more effective than “avoidance” goals. It’s important to give yourself enough time to build a positive vision of a future fund instead of simply reacting against someone else’s vision or your own prior frustrations. […]

If you can find the thing you do for its own sake, the compulsive piece of your process, and dial that up and up, beyond the imaginary ceiling for that activity you may be creating, my experience is the world comes to you for that thing and you massively outperform the others who don’t actually like hitting that particular ball. I think the rest of career advice is commentary on this essential truth.

So You Want to Start a Hedge Fund by Ted Seides [Link]

Basically the bible for anyone wanting to start a fund. I don’t even know how to possibly compress. So I advise you if you’re seriously thinking of starting a fund, getting this book should be numero uno on ya list.

Successful hedge funds are driven by the passion of their founders.

There’s also this 18-minute video:

There are almost no successful hedge funds that have equal co-portfolio managers. There are a lot of reasons why that exists and may have something to do with sort of proper delegation of responsibilities. But if you know looking at the industry that this 2-headed portfolio manager monster is almost extinct it probably makes sense not to start your business with that model. And yet you see lots of startups that are friends that got together people who used to share ideas with each other that seek out to have to equal portfolio managers and allocators hate it because it almost never works.

[…] from potentially egos getting in the way, to people who don't aren't fully in sync on their portfolio decision making process. But sometimes you don't really know until you hit a period of stress. And it might be a period of stress in the markets or a period of stress in the business and other times you see it work for a number of years until you hit that period of stress.

Also, Ted, I love you and your work, don’t get me wrong. But that YouTube thumbnail is an absolute stitch up.

On Being an Emerging Manager: Experiences, Lessons Learned, Success Factors [Link] [Apple Link]

Listened to this a few weeks ago on my trip up to Exmouth and polished it in one hit it was that good. Elliot, Phil, and John cover a wide range of questions relating to being an emerging manager. Found it interesting in the latter half of the conversation when they talk about how allocators and endowments can often string you along as an emerging manager. They’ll often take advantage of the fact that you’re keen to take on new money, using you only to get access to your strategy and information, and then ghost you or make up a bullshit reason at the last hurdle. Disappointing, yet not surprising. Reminded me of what Dan McMurtrie said: (link is below under further Resources)

Potential clients can be the worst human beings on the planet and you got to be prepared for some really odd and bad behavior

Investing is not as hard as we think [Talk] [Slides]

Found this presentation thanks to the mention in the above podcast! Awesome PowerPoint by Mark Walker of Tollymore Investment Partners that covers some of the advantages of emerging managers compared to larger institutional investors. Recommend having a quick geez through the slides at least! Loved the points on communication as investment managers:

Write involved, long shelf life letters to partners.

Write about the fundamentals of the businesses you own and why you own them.

Don’t write about market or stock price movements, nor offer explanations for these to encourage business owner mindset.

Write infrequently or ideally irregularly, dictated by having something to say rather than industry norms.

Don’t pitch ideas but write research which collects and assembles facts, data and logic.

Profit from the narrative fallacy by specifically seeking out stocks without good stories, or those with bad stories. This, rather than rates of growth and P/E multiples, is the essence of value vs. glamour investing.

Because:

What we're trying to do as investment managers is create not only a an investment track record, but a decision-making track record over time.

Finding an Edge [92 mins]

Brian Bares talks about building a moat around the investment process. Flip that question, and ask “How would you build something that’s easy to execute?”. You’d have an investment process that’s easy to execute e.g simple screens, rely on industry-standard tools like Bloomberg and watching CNBC, be excessively diversified, and be susceptible to being influenced by others.

He mentions you need to make hard choices and doing hard work. Hard choices, easy life. Easy choices, hard life.

Concentration is hard. Why is it hard? Because it's really embarrassing when it doesn't work

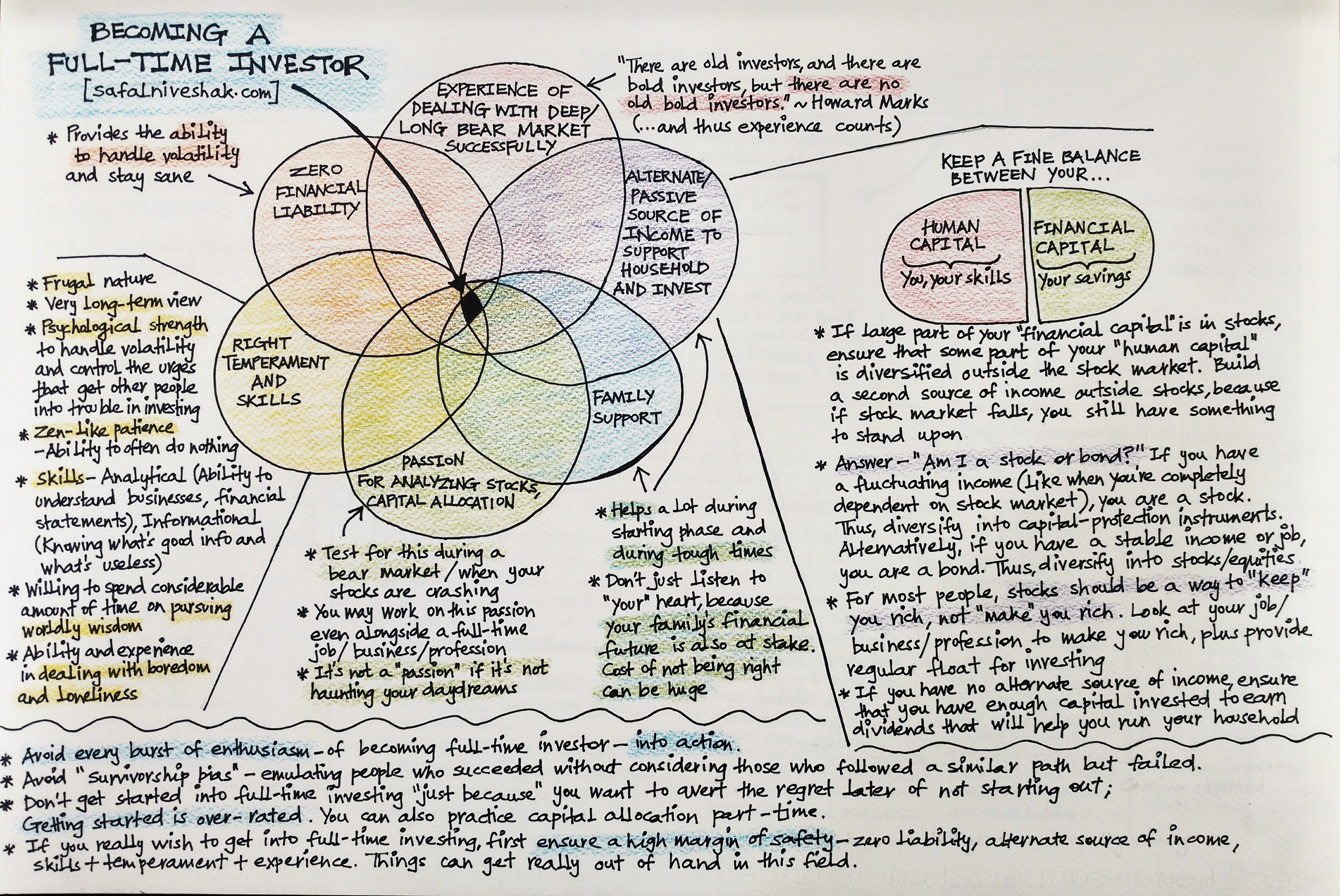

Want to Become a Full-Time Investor? Here’s Your Checklist [Link]

Safal Niveshak (@safalniveshak) with another awesome graphic. I wish more people did these.

It’s not a ‘passion’ if it’s not haunting your daydreams

How to Start a Hedge Fund - A CEO's Guide [19 mins]

Super transparent which is cool to see. Super detailed about choosing service providers, legal structures of HF’s, and fee structures.

There are a lot of angry gatekeepers in the world in general but especially in the hedge fund universe. For whatever reason, these are people who tell you stuff like “wait till you have decades of experience before launching a fund”, “wait till you retire and have gray hairs before launching” […]

Ken Griffin started citadel from a dorm room. Now of course all of these people who are successful that you hear about in the news, these are all exceptions to the norm. There's a huge survivorship bias in this industry, so even for me take my advice with a grain of salt here.But finance is not a winner take all industry. And that's really important to understand. Because there's JP Morgan, Morgan Stanley, Goldman Sachs, UBS, they all coexist amongst one another. It's designed so that there isn't one winner that just kind of dominates the entire industry and that's an amazing thing.

Further Resources:

A Guide to Institutional Investors’ Views and Preferences Regarding Hedge Fund Operational Infrastructures [Link] A mouthful of a title. And a fairly technical and niche document. But for those seriously thinking of starting a fund, this essentially outlines views and expectations to operational and organisational issues of funds.

Why Starting a Hedge Fund Is Like Opening a Restaurant [Link]

How to Start a Hedge Fund – and Why You Probably Shouldn’t [Link]

How I Started My Hedge Fund by Dan McMurtrie (Video) [Link] Great interview.

Attempting the Impossible by Neckar [Link] Awesome advice and explains the business well.

Bonus Quirky Content

Something to read: Five Lessons from History [Link]

I mean, I’ll give you the lessons. But if you truly want to understand the reasons you're probably better off reading the full thing.

the more specific a lesson of history is, the less relevant it becomes. That doesn’t mean it’s irrelevant. But the most important lessons from history are things that are so fundamental to the behaviors of so many people that they’re likely to apply to you and situations you’ll face in your own lifetime.

Lesson #1: People suffering from sudden, unexpected hardship are likely to adopt views they previously thought unthinkable. - This article was before COVID, so a perfect example.

Lesson #2: Reversion to the mean occurs because people persuasive enough to make something grow don’t have the kind of personalities that allow them to stop before pushing too far. - Basically, personality traits that push people to the top also increase the odds of pushing them over the edge.

Lesson #3: Unsustainable things can last longer than you anticipate.

Lesson #4: Progress happens too slowly for people to notice; setbacks happen too fast for people to ignore. - Good things take time. Things can go to shit real quick. E.g building a reputation.

Lesson #5: Wounds heal, scars last. - E.g. people who grew up in The Great Depression. Even as things prospered, there was always a sense of caution and frugality.

Something to watch: Illusions of Time [31 mins]

Not often a video makes you step back and say “Woah”. The idea behind prospective time vs retrospective time in the context of exciting vs boring events is so damn interesting. Basically, boring events take forever, like an airport delay, but your memory of it will be probably nothing. Whereas a 7 day holiday feels like it flys by, but you remember so damn much of it.

one of the greatest hoodwinks we ever pulled on ourselves was not noticing that the things we do to save time leave us with less of it and more alone in it

E.g One benefit of cars is that they allowed us to travel faster to work and school compared to walking. But it had the follow on effect that we now live further away from everything, whilst still having a commute time.

Something to listen to: Grant Williams on What Got You There [Link] [Apple Link]

This one’s a banger. Once every few months I find a podcast episode where I know it’s going to be re-listened to a lot. 20 mins in I knew this was one of them. Might be a little biased in liking this one because Grant has forged a path that I’m (arrogantly suggesting) extremely early on I think. And also relate to him heavily in saying he’s struggled with being a great salesman. I mean seriously, I’d struggle to sell meth to an addict. When pumping my tyres I can usually manage to mention I have a newsletter, but my elevator pitch and value proposition are seriously lacking. At best I can manage “I enjoy reading, writing, and sharing about investing’. I’m betting a kid in kindy could do better.

Life comes at you fast and things happen to you and what I’ve found over the years is it’s great to have a plan, it’s great to have somewhere you want to be in and a career path you want to follow. In the same way it’s very dangerous because if you get absolutely set on that and intent on following that course, you can be blind to things that come along that could take you in a completely different direction

Something to listen to (from me): Chong Ser Jing on Compounding Curiosity [Link] [Apple Link]

Ser Jing has a super interesting story that started with writing articles for The Motley Fool, before leveraging that into running his own fund. Some great advice for anyone thinking of going down the path as a creator -> managing money in a similar vein to Harry Stebbings or Packy McCormick.

I see a lot of problems that happen when people are not able to be comfortable being alone. And by comfortable being alone means really being able to love themselves as a human being.

Rabbit hole/resource to dive into: Memos [Link]

Sriram Krishnan has done a great job of collecting internal tech and business memos. Sam Hinkie's resignation letter and Mark Zuckerberg negotiating with Kevin Systrom over the Instagram acquisition are particular favourites of mine.

Final thought for the week:

Until next week, have a good one!

- Ksizzle

You can find previous issues of Curated by Kalani here. I’m on the web at kscarrott.com, interviewing at Compounding Curiosity, and on Twitter @scarrottkalani.

FYI: You can always hit ‘Reply’ to this email and it’ll be sent to me and I’ll reply back! Always keen to hear from readers :)

Liked this post? Why not sign up.